The Moat and Lessons Learned From Industry

17 June 2026 - A Weekly Publication by New North Ventures

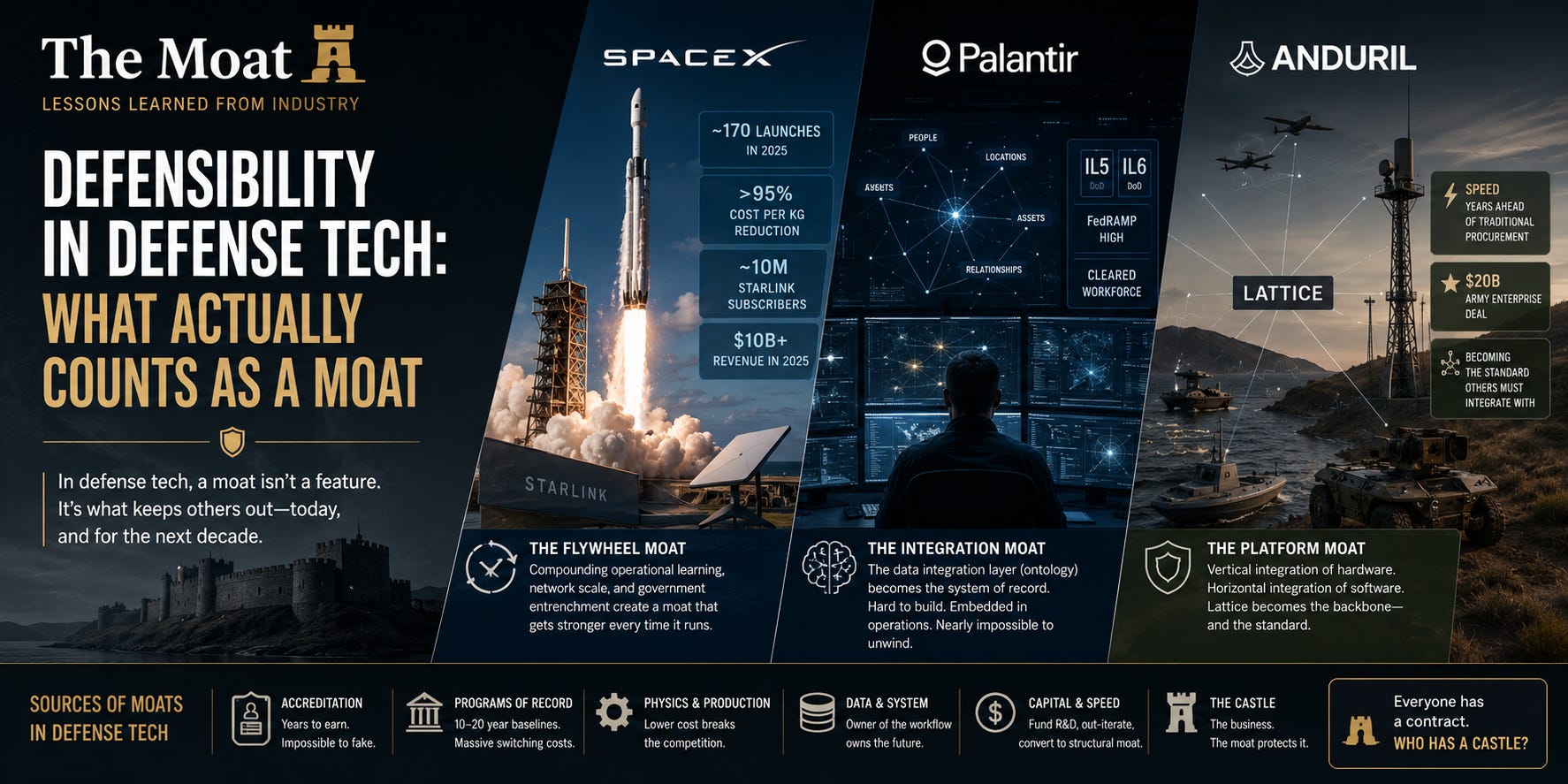

Defensibility in Defense Tech: What Actually Counts as a Moat

The question to ask nearly every founder, and if you’re a founder, ask yourself, is this: “if this works, what stops the next ten teams, and the primes, from doing the exact same thing in eighteen months?”

If the honest answer is “nothing but execution,” you’re looking at a feature, not a company. If the answer is “years of qualification, a proprietary process, a supply chokepoint, or physics most teams simply can’t replicate,” then we can start talking about a moat.

So what is a moat? Warren Buffett’s framing still holds: the business is a castle, and the moat is what keeps attackers out. In venture, you’re not underwriting whether something is good today, you’re underwriting whether returns survive once the market realizes it’s a good market. Without a moat, margins collapse as competition floods in. A moat is what prevents capital and talent from simply taking your customers.

The classic sources still apply such as IP, switching costs, network effects, scale advantages, regulatory barriers. However, defense bends them and adds a few that the commercial world rarely has:

Accreditation – One of the most underrated barriers in the sector. Clearances, FedRAMP High, DoD IL5/IL6, ATOs, weapons qualification. These take years and millions in “paperwork” that is actually infrastructure. You cannot fake a cleared workforce or accredited facility; it is a decade long build. Palantir is one of only a handful of companies, alongside Microsoft and AWS, cleared at DoD IL6. That’s not a feature; it’s a locked gate.

Programs of Record – Defense procurement is sticky in a way commercial markets aren’t. Win a program of record and you become the baseline for 10–20 years. Switching costs aren’t churn, they’re full system re-architecture.

Physics and production – If you can deliver something cheaper than anyone else, competition doesn’t erode you, it breaks everyone else. This is the SpaceX story, and increasingly true in maritime and munitions.

Data – Whoever becomes the system of record owns the workflow. Once you define the data model, ripping it out means rebuilding the entire operating picture.

Capital – Cost-plus primes have little incentive to move fast. Startups that fund R&D on their own balance sheet can out-iterate incumbents, until that speed is either converted into a structural moat or it disappears.

Now let’s look at a few winners, because each illustrates a different moat and most stack multiple.

SpaceX

The lazy take is that SpaceX’s moat is reusable rockets. It isn’t anymore. Blue Origin landed an orbital class booster in 2025, and others are close, proving the physics is replicable. The real moat is compounded operational learning that only cadence can create.

SpaceX flew ~170 times in 2025 across nearly 500 total missions, driving cost per kilogram down more than 95%. Every flight improves refurbishment, reliability, and mission design in ways competitors can’t replicate without the same flight volume. The flywheel reinforces itself: cheap launch enables Starlink, Starlink fills the manifest, and a full manifest funds more cadence.

On top of that sits Starlink: ~10 million subscribers and $10B+ in 2025 revenue, with improving margins. That creates a network and capital moat layered on launch dominance. Then comes government entrenchment: NSSL backlog, NASA contracts, and Starshield positioning it as default infrastructure for national security space access.

As SpaceX approaches a ~$1.77T valuation in private markets, the signal is clear: these moats compound.

Lesson: durable advantage isn’t a feature, it’s a loop that gets stronger every time it runs.

Palantir

Palantir is often misread as an AI company. It isn’t. It uses other people’s models such as OpenAI, Anthropic, and others.

The real moat is the data integration layer: Foundry and Gotham. It is a semantic ontology that maps how an organization’s fragmented data actually fits together. Building it takes 6–18 months. Once it exists, switching AI vendors is trivial but rebuilding the ontology elsewhere is a multi-year reintegration effort most organizations won’t attempt.

That layer becomes embedded in daily operations. Removing it would break the system.

Wrapped around it is accreditation: FedRAMP High, IL5/IL6, and a cleared workforce. Palantir turned that burden into a product with FedStart, letting others operate inside its accredited environment instead of rebuilding their own ATO path. That converts compliance into a platform advantage.

The moat is the integration layer and it outlives whatever model sits on top of it.

Lesson: be the system of record, not the application. Apps get replaced. Data models do not.

Anduril

Anduril is often described as a modern prime, but it is structurally anti-prime. Traditional primes rely on cost-plus contracts that reward neither speed nor efficiency. Anduril flipped the model: hardware is the delivery mechanism for a software platform.

Lattice is the core: it fuses sensors, drones, towers, and effectors into a unified operating system. The result is a vertically integrated system with a horizontal software engine, one backbone across many hardware classes.

The second moat is speed-as-capital. By funding R&D privately, Anduril reaches deployment years ahead of traditional procurement cycles. That’s how it secured a $20B Army enterprise deal consolidating 120+ procurement pathways around Lattice.

The third moat is emerging: Lattice as a standard. As it becomes the integration layer, competitors either plug in or get excluded from systems built around it.

Lesson: if you sell hardware, find the recurring software layer or become the standard others must integrate with.

How to build real moats

Start the boring barriers early. Clearances, ATOs, accreditation, qualification. Build them before you need them. They look like cost today and a moat tomorrow.

Use capital and speed deliberately. Outspend incumbents on R&D and convert that speed into structural advantage before the capital edge fades. Speed is a moat with an expiration date.

Don’t confuse contracts with moats. A contract is an outcome. A moat is what ensures the next one.

The defense boom is real, and it’s producing winners faster than ever. But the companies pulling away all share the same pattern: compounding cadence, integration layers others can’t unwind, and standards everyone else must adopt.

Everyone has a contract. The question is: who has a castle.

Anthropic Disabled Fable 5 And Mythos 5 After A U.S. Export-Control Order. Here What Happened

Anthropic, one of the leading frontier AI labs, has disabled access to its most advanced models, Fable 5 and Mythos 5, following a new U.S. export control order that restricts foreign access to cutting edge artificial intelligence systems. The company is now engaged in ongoing negotiations with the Trump administration to restore access, but so far no breakthrough has been reached. The move represents one of the most significant exercises of AI export restrictions to date, affecting not only international users but also raising questions about how compute thresholds, model capabilities, and national security considerations will intersect as the technology continues to advance.

The timing and scope of the restrictions are notable. Anthropic’s Fable 5 and Mythos 5 are widely considered to be among the most capable large language models available, used across enterprise, research, and government applications. By targeting these specific systems, the U.S. government is signaling that it views advanced AI as dual-use infrastructure requiring the same kind of strategic export discipline traditionally applied to semiconductor manufacturing equipment, cryptography, or missile technology. This is no longer theoretical policy. It is operational doctrine, and it marks a shift from voluntary corporate governance to direct state intervention in the AI supply chain.

More links to explore:

AI is taking background checks from ‘months to hours,’ clearance agency says

Defense Tech Funding Smashes Records: Autonomous Weapons Startups Raise $14.6B

Hubble Network, InPlay Partner to Bring Sub-$1 Global Tracking

Hubble Network and InPlay have partnered to make global, item level asset tracking as inexpensive as passive RFID by combining InPlay’s sub $1 NanoBeacon chip with Hubble’s satellite powered Bluetooth network. The solution allows smart labels, wearables, and IoT sensors to transmit location and condition data worldwide without requiring companies to deploy readers, scanners, cellular modems, or other tracking infrastructure. The partnership is aimed at supply chain visibility, cold chain monitoring, returnable transport assets, and other use cases where traditional RFID lacks range and cellular tracking is too expensive, potentially enabling low cost tracking of billions of everyday items.

Thanks for reading Securing Our Future! Subscribe for free to receive new posts and support our work.